Core bond investors have experienced one of the worst starts to the year ever, potentially calling into question the validity of bonds in a portfolio. Despite the poor start, we don’t think the value proposition for bonds has changed much. Moreover, with yields on most fixed income markets moving sharply higher, now could be a good time to revisit fixed income markets. Starting yields are still the best expectation of future returns and have become more attractive in a number of markets recently.

Has the value proposition of core bonds changed?

With most equity and fixed income markets down to start the year, a traditional 60/40 portfolio has come under pressure. Moreover, seeing both markets down simultaneously may cause investors to question the validity of a 60/40 portfolio broadly and core bonds specifically. For us, the value proposition for core bonds is that they tend to provide liquidity, diversification (to equity market risk), and positive total returns to portfolios. Unfortunately, none of those values are 100% certain all the time. Like all markets, fixed income investing involves risks and, at times, negative returns (although negative fixed income returns tend to be much smaller than negative equity returns). That said, as painful a start to the year as it has been for equity and core fixed income investors, it isn’t all that uncommon to experience negative returns for both equity and fixed income markets at the same time. In fact, since 1995, nearly 15% of monthly returns have had both negative equity and fixed income returns. Again, it doesn’t make the experience of a diversified portfolio any less painful this year, but we believe it also doesn’t change the argument to own core bonds in a portfolio.

Moreover, with the economy likely in the middle of the economic cycle, the need for high-quality bonds actually increases, in our view. That is, the need to offset potential equity market volatility remains an important role for core fixed income. Bonds, particularly core bonds, have been less volatile than stocks and have historically provided a ballast to portfolios during equity market drawdowns, which as we know, are normal occurrences from time to time. The maximum drawdown for bonds, in any given month, has been dramatically less severe than stocks. While the worst drawdown in a month for equities was -28%, the worst bonds have done during a month was lose 6%, and those losses were quickly reversed. So, when combined with equities, bonds help reduce total portfolio volatility, which makes for a smoother investment experience for investors.

It’s all about the bond math

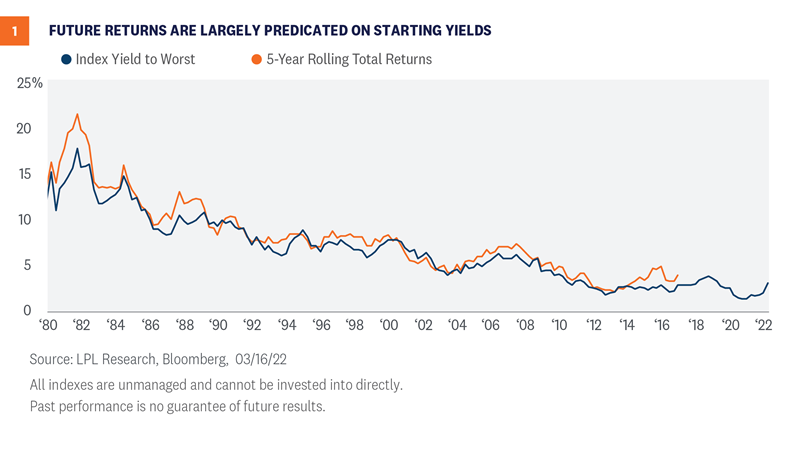

Fixed income instruments, for the most part, are unique in their structures in that, absent defaults, expected returns are largely determined by starting yields. That is, we tend to have a pretty good idea what to expect out of many fixed income instruments over time because coupon and principal payments are known in advance and are contractually obligated. As such, whether you’re invested in an individual bond, an investment that tracks an index like the Bloomberg Aggregate index [Figure 1] or a strategy designed to actively outperform an index, returns are largely predicated on starting yields. And this is true if you hold the fixed income instrument to maturity (for an individual bond) or at least five years (for a portfolio of bonds) regardless of what interest rates do in the interim.

An important point about the negative returns we’re seeing this year is that yields are moving higher because of the expectations of higher short-term interest rates and not an increase in credit risk. Fixed income markets repriced, rather quickly, the prospects of accelerated Federal Reserve (Fed) rate hikes this year. Towards the end of 2021, fixed income markets only expected one or two rate hikes this year, but in January and February, markets have priced in seven hikes this year. This quick adjustment in expectations caused yields across the curve to move higher. However, there is a huge distinction between yields moving higher due to the prospects of higher short-term interest rates versus yields moving higher because of higher credit/default risks, which could represent permanent impairments of capital.

As shown above, absent defaults, starting yields represent the best expectation for future returns regardless of what interest rates do. That is, if you buy and hold a fixed income investment, the short-term volatility you experience due to changing interest rate expectations is just volatility. It has very little bearing on the actual total return if held to maturity (or if held to the average maturity of a portfolio of bonds). If you consider the historical returns of the Bloomberg Aggregate Bond Index, the overwhelming majority of returns came from coupon income and not price returns (which is generally the opposite of equity investments). For example, over the last five years, the index returned 12.52%, on a cumulative basis, of which price volatility only detracted by -0.75% over the entire five years (and that includes this year as well). Coupon and principal payments are much more important than price volatility.

What goes down, must go up?

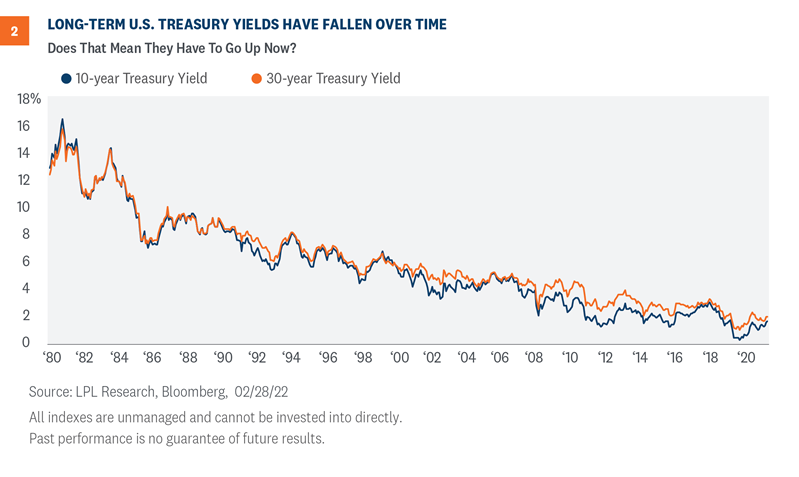

What has been characterized as a bond bull market, bond yields have seemingly only fallen from very lofty levels over the past 40 years [Figure 2]. Long-term yields peaked above 15%, in the early 1980s and have fallen to a little over 2% currently. Because interest rates are seemingly bound by zero in the U.S. (although there remains over $3 trillion in negative yielding debt globally), some investors are wondering if the only way is up for interest rates (which would mean negative bond prices). We remain unconvinced. Moreover, just because a bull market ends, either in equities or bonds, doesn’t automatically mean a new bear market must immediately follow.

However, that yields have continued to fall over time are due to a number of structural reasons, which, we think remain in place and should keep U.S. Treasury yields from persistently increasing. These factors include:

- Demographics- A primary reason for the continued march lower in bond yields, especially over the past 20 years, has been aging global demographics and, more specifically, the need for income. That hasn’t changed. The need for safe, reliable income is as high as it’s ever been and should keep yields from going too much higher.

- Global Debt dynamics- With over $225 trillion in debt globally (IMF), elevated debt levels limit economic growth potential especially as debt service costs increase. Lower interest rates are actually correlated with lower economic growth.

- Dis-Inflation- Due to a number of factors, inflation has fallen over the past 40 years. Certainly, the inflationary pressures we’re seeing now should give core fixed income investors pause and remain the wildcard for higher yields. However, with central bankers around the world embarking on rate increases to arrest high consumer prices, we don’t believe we are in a new, higher inflationary regime. Moreover, longer-term market implied inflation expectations remain well within historical ranges, suggesting inflationary pressures should abate over time.

- Flight to safety- Core bonds and, more specifically, U.S. Treasury securities continue to be the best diversifier to broad-based equity market sell-offs, which tend to happen when the economy slows or there are macroeconomic shocks. When we look at how Treasury securities have performed during periods of equity market selloffs, Treasury security returns have been mostly positive—although not every time. But in every situation, Treasury securities outperformed equities, which means an allocation to Treasury securities would have both improved portfolio returns and reduced portfolio volatility during these periods.

- Active fixed income management- With trillions invested with active fixed income managers, any move higher in yields, absent an increase in default expectations, presents an investment opportunity. Additionally, because of strong equity market returns over the last few years, private pension funds are well-funded and are actively de-risking portfolios by buying long-term bonds. According to the Organization for Economic Co-operation and Development (OECD), there are $35 trillion in pension fund assets with most of these plans fully funded. This could provide a tailwind to bond prices.

Time to buy the dip?

Firmly ingrained, at least recently, in equity investors has been this buy the dip mentality. However, it may not be as ingrained in retail bond investors although maybe it should be. As noted above, future returns, absent defaults, are largely determined by starting yields, regardless of what the interest rate and inflationary environments look like. And with yields moving higher recently in most fixed income markets, future returns for fixed income investors have improved. We’re seeing increasing investment opportunities in a number of shorter maturity securities (since yields on shorter maturity securities have moved up the most) such as short maturity investment grade corporates and Treasury securities and lower rated corporate credit. Moreover, with yields on the core bond index now back up close to its longer-term average, core fixed income broadly is more attractive.

Conclusion

Core bonds have been a staple in diversified asset allocations. However, with returns as negative as they’ve been this year, investors may be undergoing a rethink of the utility of core bonds. We think that may be a mistake. We still think the value proposition for core bonds remains. Liquidity, equity diversification, and total returns are all valuable properties core bonds bring to diversified portfolios. Moreover, bonds are unique in their structures in that coupon and principal payments are, for the most part, guaranteed and the primary factors of long-term total returns. The price volatility we’ve seen so far this year doesn’t impact those payments. And with yields higher in many markets, now may be a good time to start looking at additional investment opportunities within fixed income.

Click here to download a PDF of this report.

______________________________________________________________________________________________

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

| Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value |

RES-1094501-0322 | For Public Use | Tracking # 1-05257812 (Exp. 3/23)